We are seeing a lot of activity in Commercial Mortgages – both owner-occupier and investment – and just like with a personal mortgage it is logical to think that one of the primary things that a lender will look at is whether you can afford to repay the mortgage – both now and in the future.

We want to cut through the acronyms and smoke and mirrors to show that far from being some sort of ‘dark arts’ it is the same process they use to evaluate your business as we all might do our own personal finances.

With a Commercial Investment Mortgage the maths is relatively straightforward; you will have a commercial lease in place with your tenant and the lender will ‘stress’ your mortgage with simulations of interest rate rises to ensure that even if rates were to rise from their current levels then the commercial lease still makes the mortgage payments affordable.

Commercial Mortgages for trading businesses have far more moving parts as affordability is based on the future trading performance of the business.

In the absence of a crystal ball the lender has to use past performance as a guide to whether your business can service the mortgage moving forward.

Again we can draw a similarity here with a personal mortgage application – your prospective lender would want to know all about your income, together with the other debt and outgoings that you have to service regularly. From this they will derive how much ‘headroom’ you have in your finances to be able to afford the mortgage.

Debt Coverage Ratio (DCR)

I did say that we wanted to cut through the acronyms – so it’s high time that we started to use them!

When a lender takes away your outgoings for debt from your income, they will be left with the current ‘headroom’ in your finances from which your company’s mortgage can be paid moving forward. But there are still variables in this number such as your business turnover decreasing, or your other costs or debt increasing.

So the lender won’t want to see that your headroom is equal to (or less than) your future mortgage payments, but a multiple of them. This is called your Debt Coverage Ratio (DCR) – and commonly lenders are looking for a DCR of 1.5x to 2x.

Calculate your Debt Coverage Ratio (DCR):

Annual Net Income Divided By Annual Debt Payments = Debt Coverage Ratio

For example:

£82,500 Net Income Divided By Annual Debt Payments £45,000 = DCR of 1.83

Using the ‘right’ Net Income

Of course it couldn’t be so easy that the lender could just cherry pick a line from your company’s last set of filed accounts and use that; oh no, they have to go and make us calculate another number that they use in their affordability calculations too!

Your existing company accounts include existing lease or mortgage payments but the lender is evaluating future affordability of a new mortgage – so the ‘net income’ that they use will have certain items added back onto it.

This generates what lenders generally call ‘adjusted net profit’ or ‘adjusted EBITDA’.

We are not qualified accountants, so these calculations really do stay on the ‘back of an envelope’ for our purposes. In simple terms take the profit before tax and add back to that items such as:

- Lease / Rent

- Depreciation

- Amortisation

- Directors’ Dividends

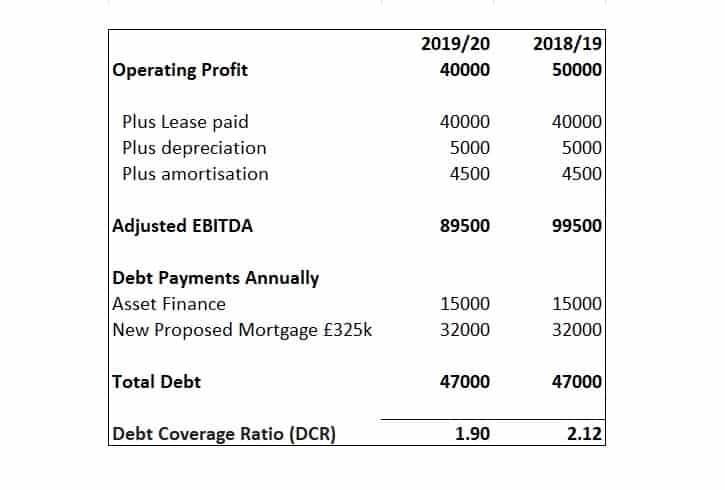

Case Study – ABC Ltd

We can take the case of ABC Ltd, and then put into practice the above construction of the Net Income, and then use that along with the debt in the company to derive their Debt Coverage Ratio (DCR).

- ABC Ltd. currently pays £40,000 pa commercial lease

- Annually ABC Ltd. make £15,000 in Asset Finance payments

- They are applying for a 70% LTV mortgage on a £465,000 purchase price, meaning a £325,000 loan, estimated by the lender to be £32,000pa initially in annual payments

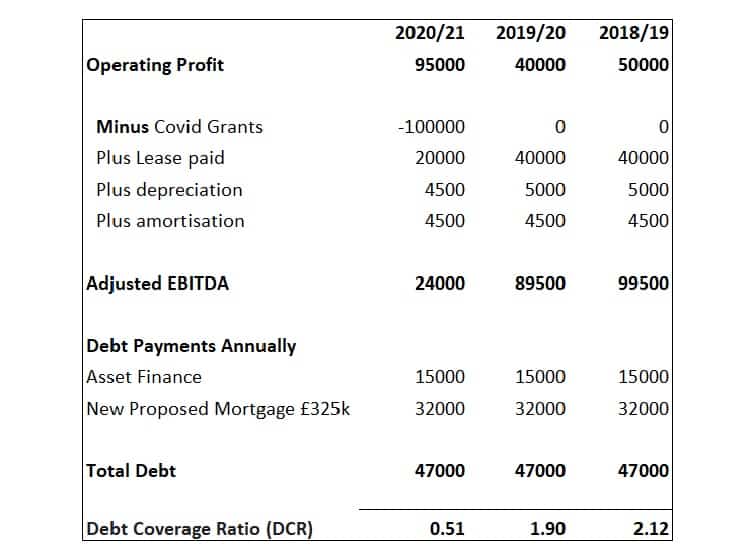

Accounting for the pandemic impact

Like a lot of businesses in the country, ABC Ltd was Covid impacted, and so if we moved forward to the current period, and included the financial year 2020/21, then that doesn’t present on its own a Debt Coverage Ratio (DCR) that the lender would see as indicating affordability.

The obvious addition to this table is the fact that the lender will strip out Covid related grants and income that are one off in nature, and this reduces the DCR to levels where the lender would not arrive at a positive decision for affordability.

But we are now a few months into the next financial year, and thankfully into recovery mode for many business post-pandemic restrictions, and so lenders are willing to include the accounts for this new current financial year in their assessment.

The April to June quarter 2021 actually showed a 25%-30% increase on turnover compared to the 2019 and 2018 figures for the same months, and so there is something here for the lender to work with and progress for ABC Ltd.

We are seeing a lot of demand for, and activity in, Owner-Occupier Commercial Mortgages – and armed with the accounts and facts we can work with lenders to find suitable and affordable solutions for the roof over your business.

How do you want to get funded?

Mark Grant, July 2021.

info@fiduciacommercialsolutions.co.uk / 01636 614 014